OBBBA and the Exempt Sector: What Trade Associations and Nonprofits Must Know Now

The One Big Beautiful Bill Act (OBBBA) has generated significant commentary around its manufacturing incentives and corporate tax provisions. For finance leaders at 501(c)(6) trade associations and 501(c)(3) nonprofits, however, the legislation carries a separate set of implications—ones that demand immediate attention rather than a wait-and-see approach.

Several provisions within the OBBBA directly reshape how exempt organizations manage compensation, fundraising strategy, and investment income. As the Assurance Partner at Kellogg and Kellogg, PC, I lead the firm’s audit practice and specialize in guiding trade associations, nonprofits, and other industries through their unique financial and operational challenges. In this article, I’ll walk you through the sections most likely to affect your organization's financial operations as of 2026—and what your board and finance team need to audit now.

The Expansion of Section 4960: A Compliance Burden That Grows Over Time

Of all the OBBBA provisions affecting the exempt sector, the expansion of the Section 4960 excise tax carries the most significant long-term administrative weight.

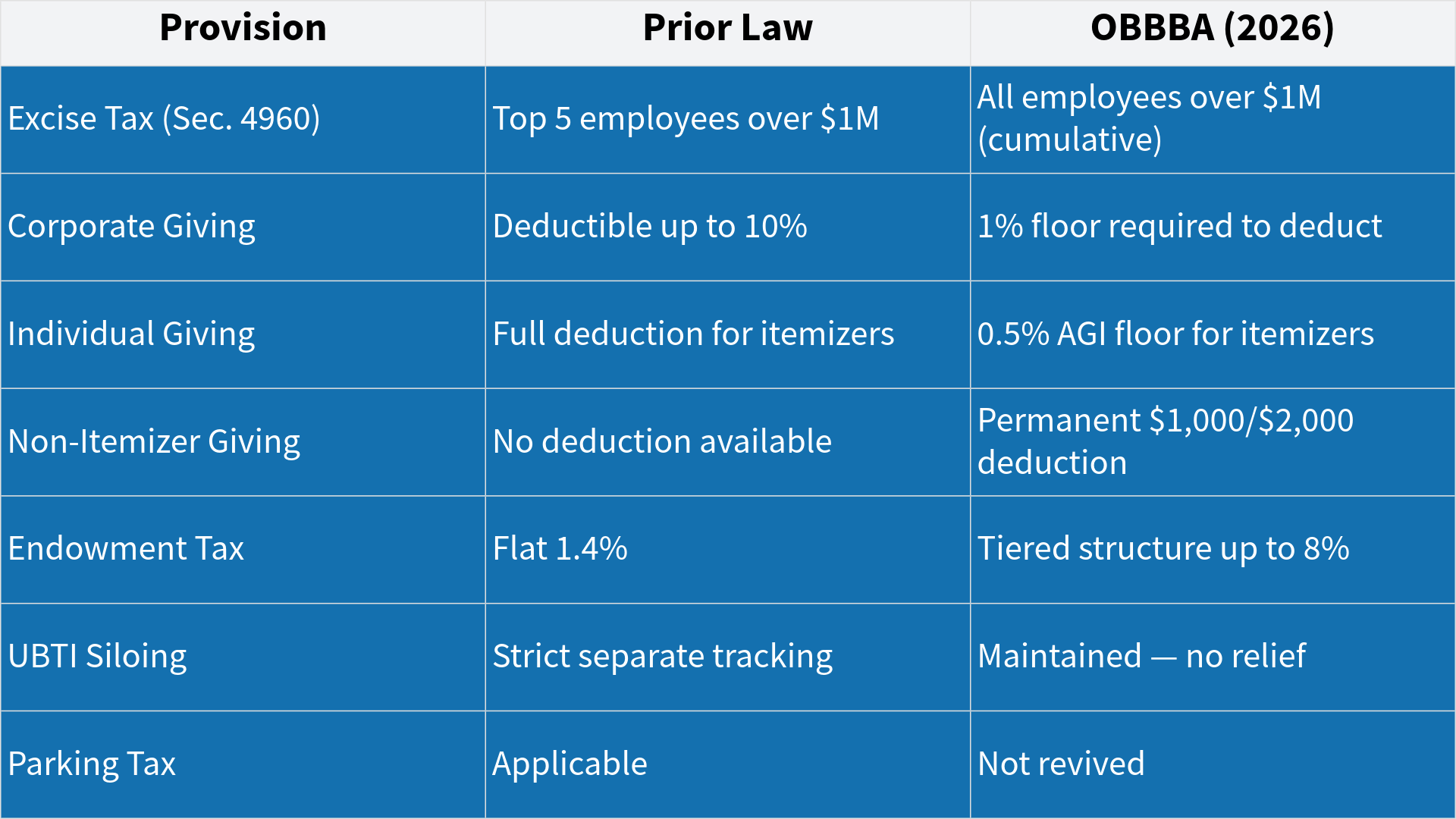

Under prior law, the 21% excise tax on compensation exceeding $1 million applied only to an organization's top five highest-paid employees. Section 70416 of the OBBBA removes that cap entirely. The tax now applies to any current or former employee who receives more than $1 million in compensation in a given taxable year—with no ceiling on the number of individuals covered.

What makes this provision particularly challenging is the "permanently covered employee" rule. Any individual who qualified as a covered employee in any tax year beginning after December 31, 2016, retains that status indefinitely. This means your organization must now maintain a cumulative, ever-growing list of individuals—including former employees who may have departed years ago—for whom excise tax exposure could arise on deferred compensation payments or severance arrangements.

For associations with long tenures and competitive executive compensation structures, this is not a theoretical risk. It is an active compliance obligation that requires a dedicated tracking system and a review of all existing compensation agreements.

Action step for finance teams: Conduct an immediate audit of all current and former employees who have met the covered employee threshold since 2017. Evaluate deferred compensation schedules and severance agreements for potential excise tax exposure.

New Floors on Charitable Deductions: Rethinking the Donor Conversation

The OBBBA introduces deduction floors that change the tax calculus for your donors—and, by extension, your fundraising strategy.

For individual itemizers (Section 70425): Charitable contributions are now only deductible to the extent they exceed 0.5% of a donor's Adjusted Gross Income (AGI). For a donor with a $200,000 AGI, the first $1,000 of giving generates no tax benefit. Only contributions above that threshold become deductible.

For corporate donors (Section 70426): A 1% floor applies. Corporate donors may only deduct charitable contributions that exceed 1% of their taxable income. The existing 10% ceiling remains in place.

The practical implication for trade association foundations and 501(c)(3) organizations is straightforward: small-dollar corporate sponsorships may no longer provide a meaningful tax benefit to the donor. Appeals built primarily around deductibility will carry less weight for this segment of your donor base.

This is the right moment to reframe your donor communications. Emphasizing mission impact, organizational outcomes, and community value will serve organizations better than leading with tax incentives—particularly for contributions that fall below the applicable floor.

A word directly to boards: As you look ahead to 2026-27 fundraising projections, these floors deserve serious consideration. For any donor whose typical gift falls near or below the AGI threshold, your development team should prepare for potential giving reductions and develop a strategy that centers impact over deductibility.

The Permanent Universal Deduction: A Win for Mid-Level Giving

Not every OBBBA provision works against the exempt sector. The permanent establishment of an above-the-line deduction for non-itemizers represents a meaningful opportunity—particularly for organizations that have historically struggled to engage the broad middle tier of American donors.

Under this provision, individuals who take the standard deduction may now deduct up to $1,000 in cash contributions ($2,000 for joint filers) directly from their gross income. This benefit is permanent, not temporary.

The significance of this provision is difficult to overstate. Approximately 90% of American taxpayers currently take the standard deduction. For years, those individuals have had no tax incentive to give to charitable organizations. That barrier has now been removed—at least for the first $1,000 or $2,000 of giving.

For nonprofits and association foundations with active mid-level donor programs, this provision opens a new lane. Solicitations targeting the standard-deduction majority can now include a genuine, if modest, tax benefit as part of the case for giving.

What Did Not Change: A Note on UBIT and the Parking Tax

There is some relief worth noting. The OBBBA did not revive the widely criticized "parking tax" that previously increased Unrelated Business Income for transportation fringe benefits. The proposed expansion to tax royalties from name and logo licensing also did not move forward.

The siloing rules for Unrelated Business Taxable Income (UBTI) remain intact. Associations must continue tracking each separate trade or business independently—no consolidation relief was included. This is not new, but it is worth confirming that your current tracking methodology remains compliant.

OBBBA Changes at a Glance: Summary for the Exempt Sector

Prepare Before the Provisions Take Full Effect

The OBBBA provisions outlined above are not speculative—they represent the operating reality for exempt organizations beginning in 2026. The organizations that respond most effectively will be those that conduct a structured audit of their compensation records, donor programs, and investment income classifications now, rather than discovering gaps during the year-end review.

If you're a CFO, controller, foundation or trade board member, or finance leader, our LinkedIn newsletter version of the Kellogg Ledger tailored just for you. Subscribe to get every new issue delivered directly to your feed.

Dina Kellogg, CPA, is the Assurance Partner at Kellogg and Kellogg, PC, where she leads the firm’s audit practice. She provides high-quality financial statement audits and reviews for nonprofit organizations, trade associations, and companies in the construction, manufacturing, and other industries.

Her insights contribute to Kellogg and Kellogg's thought leadership, offering actionable advice on financial oversight, governance, audit readiness, and strategic planning for nonprofit boards, trade associations, and other industries.

All content shared here is for reference and general information only. It is NOT tax, legal, or financial advice. Decisions about tax and financial matters require personalized professional attention. Readers should contact Kellogg and Kellogg or their current tax advisor for specific guidance.